Recent

Recent

© Sebastian L | Dreamstime.com

Top Stories

Top Stories

Photo 264179951 © Yee Xin Tan | Dreamstime.com

Recommended

Recommended

© Golubovy | Dreamstime.com

© Paul Cowan | Dreamstime.com

© Arne9001 | Dreamstime.com

© Brian Lasenby | Dreamstime.com

Dreamstime

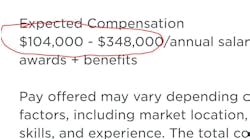

Members Only Content

© Lightfieldstudiosprod | Dreamstime.com

© Endostock | Dreamstime.com

© Spaxia | Dreamstime.com

Continuous Improvement

Fix Your Just-in-Time Engine

April 17, 2024

© Navee Sangvitoon | Dreamstime.com

© Olivier Le Moal | Dreamstime.com

© Richair | Dreamstime.com

© Piotr Swat | Dreamstime.com

© Sensay | Dreamstime.com

Coca-Cola Co.

© Yuryz | Dreamstime.com

Members Only Content

Innovation

Is Your Intellectual Property Under Attack?

April 23, 2024

© Yukchong Kwan | Dreamstime.com

Photo 137592009 | 5g © Ekkasit919 | Dreamstime.com

Members Only Content

Siemens

R.A Jones

Courtesy of ABB

© Alexandersikov | Dreamstime.com

Featured Media

Featured Media

IndustryWeek

IndustryWeek

ID 202424474 © Alendimion | Dreamstime.com